The market is up, but how are our gaming tokens doing?

GC ALPHA 58

Disclaimer: None of this information should be taken as financial advice. DYOR + I will hold some of the assets mentioned in this newsletter.

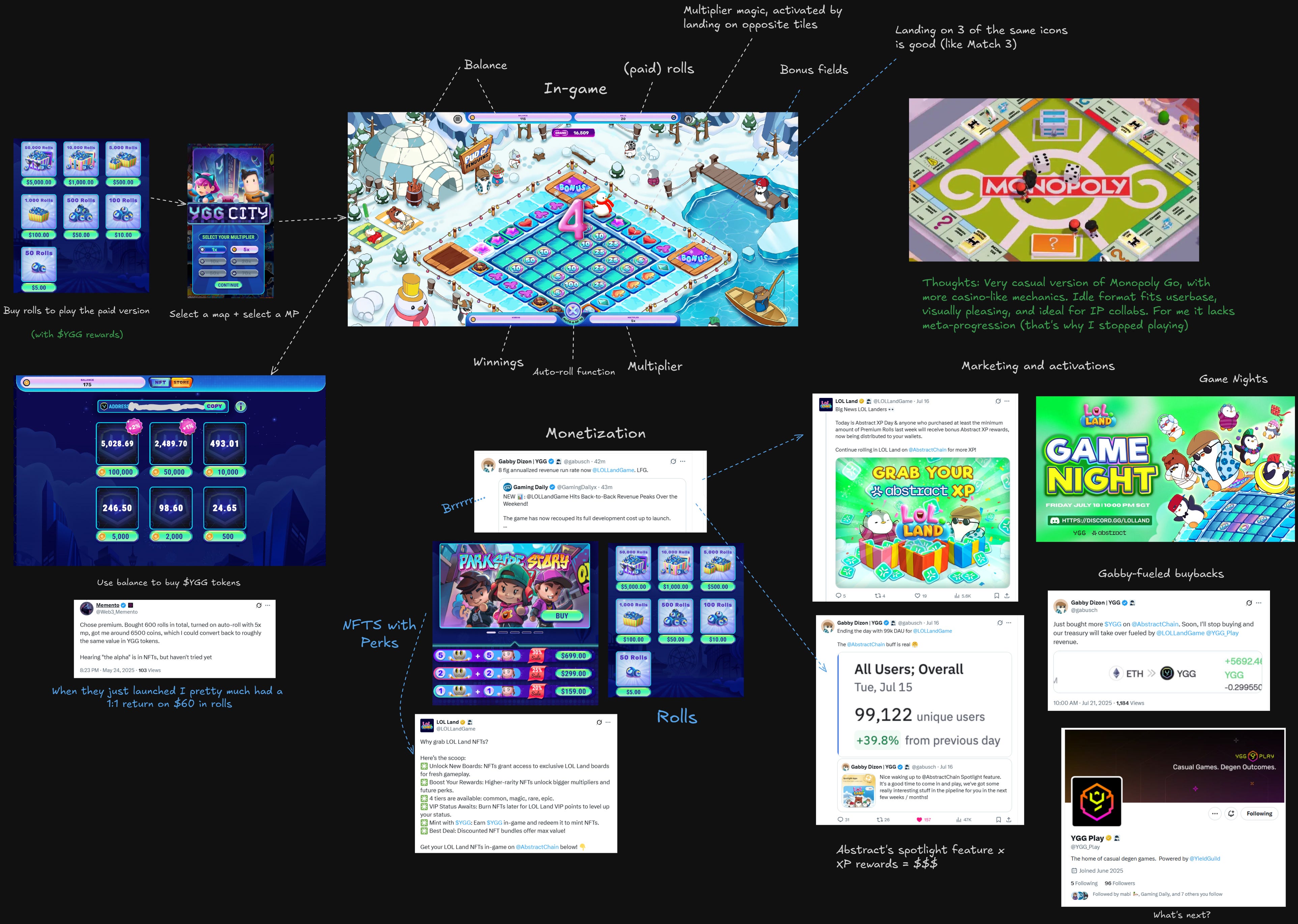

PRODUCT REVIEW: LOL.Land

In light of Raiden officially joining YGG, I wanted to share some thoughts on LoL Land, presented in a new and more visual format (experiment):

Next week, we will explore …..

MARKET TALK

A NEW VISION TO RALLY BEHIND?

In 2021 - 2022, during the "gamefi cycle," we experienced a gold rush of new opportunities, driven by apps like Axie. And more importantly, we rallied behind a common vision: the metaverse

Gaming was well-positioned to benefit from this potential future, leading to a massive influx of speculative capital from retail and VCs. Tokens like Decentraland, The Sandbox, and Illuvium received billion-dollar valuations (it was so different back then...)

But as the years passed, the “metaverse dream” has crumbled. More recently, the cracks in the foundation that was built on this dream have started to widen:

Multiple shutdowns, studios not being able to raise, 50+ failed TGEs, etc.

Since we haven’t had a vision of the size of the metaverse, a supposed “multi-trillion dollar opportunity”. There hasn’t been another dream for CT and retail to believe in, and I wonder if there’ll ever be another one of that size

This lack of a broader vision, while we have little to show for the amount of capital that was infused in the sector, likely left a sour taste in many people’s mouths

We did have a small spike of interest in the intersection of AI x gaming over the last year, and the tools have rapidly improved since then (e.g., Remix GG). Maybe, as these tools become more impactful, we’ll start seeing change

Or maybe, there’s a future for multi-billion-dollar onchain economies, albeit smaller than the metaverse

Maybe the metaverse is still something achievable, who knows?

The belief in the metaverse is gone, and slowly, the industry seems to be returning to fundamentals (“the revenue meta” lol). This cleanse comes with a lot of pain, but it is also healthy to see maturation

So, will we find a new vision and see speculative capital return, or will a more fundamental approach become the standard moving forward?

TGEs UPDATE

It’s been a while since I provided an update on the gaming token sentiment through the lens of TGEs in 2025 (update from June 1st). So, here’s a new (yet disappointing) update:

Total launches ~65 (tracking 51)

16/50 (32%) of tracked tokens launched since June 1st

Average 24h volume: ~$26M

When excluding the top 3, this becomes only $3.1M (-88%). Do note that OIK’s 24h volume is exceptionally high ($715M) for some reason

Average decrease of the market cap of 67% compared to the ATH

In the June update, this number was 69%. The lack of change despite improved macro conditions seems largely fueled by “dead” tokens continuing to lose relevancy, and therefore shrinking in market cap, + lack of improvement for the new, larger MC tokens

On the first point: tokens with a market cap of ~$2M or below have increased by 10 tokens (from 12+ to 22+ regarding tracked tokens)

The largest token by market cap and FDV remains NXPC: $200M / $1.07B

According to CMC data, the overall market cap of all gaming tokens is $22.6B. This number was $23.93B on the 1st of January 2025

YoY we’re up only 3.3% in market cap, but 123% in volume. Looking at the recent trendline, it looks like we’re headed for significant market cap growth, fueled by ETH’s recent performance

However, much of that growth/liquidity seems to be fueling the legacy or established tokens, with a few exceptions like CROSS, NXPC, and OIK

Overall, it’s not looking too pretty for new gaming TGEs yet, and we have yet to see if an altcoin run could lead to → more confidence in new tokens. Nevertheless, the overall gaming market seems to be poised for growth

ON THE RISE

WilderWorld introduces Operation Titan: a major buyback plan

Opinions.fun is a new “opinion marketplace” on Solana, powered by Kaito